Bankrupt FTX announced today that it was able to locate around $1.5 billion in assets worldwide.

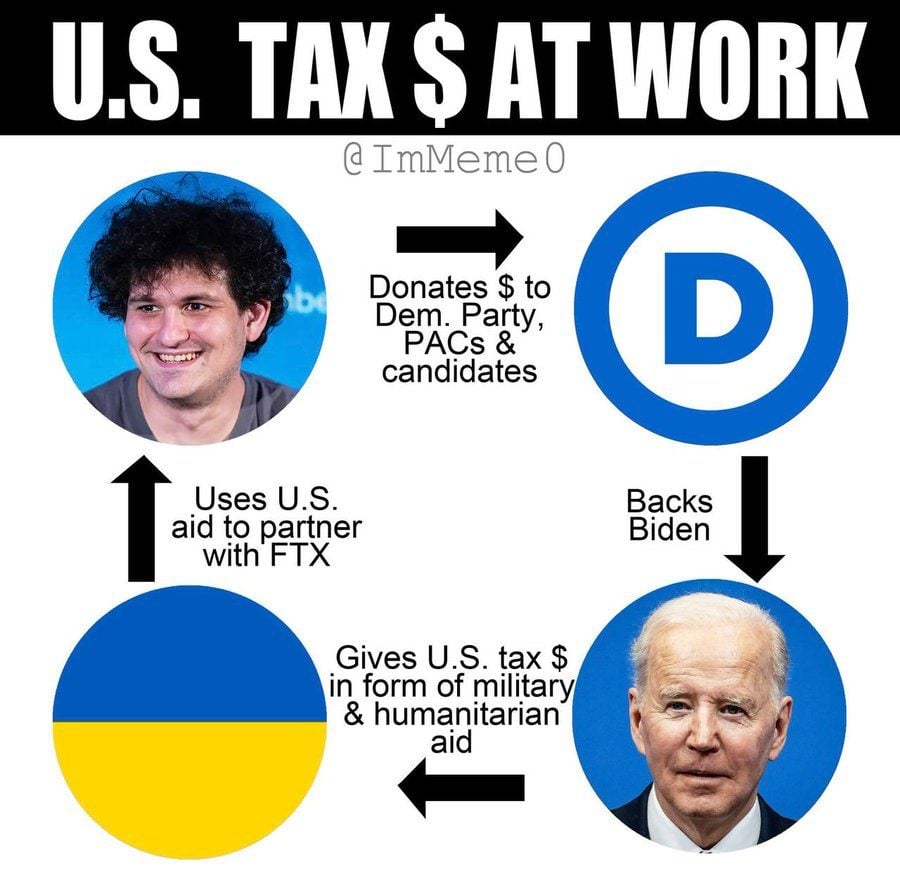

FTX went bankrupt a couple of months ago. The company was involved with millions going to corrupt mostly Democrat politicians.

We also quickly learned that FTX was involved in Ukraine and the Ukraine government had invested in FTX with money sent to Ukraine from the US.

Democrats’ “Newest Megadonor” Loses Billions As Crypto Exchange Fails — “Dot-Com Bust Level Event”

We know FTX was used as a conduit to move money from Ukraine to US politicians. We don’t know how much.

The new leadership in FTX is trying to get their arms around how much money the company has and how much it lost.

FTX executives are currently trying to claw back hundreds of millions of dollars in cash from hundreds of bank accounts as they seek to resolve the position of the collapsed crypto exchange, its creditors were told Tuesday.

The company’s new management, which took over when FTX founder Sam Bankman-Fried resigned Nov. 11, told a procedural hearing on Tuesday that it had over $1 billion in assets identified. The company located about $720 million in cash assets, which the exchange has yet to consolidate, in U.S. financial institutions authorized to hold funds by the U.S. Department of Justice. Another near $500 million is already being held in U.S. institutions.

“We are reaching out to all of those banks and changing the signatories on the accounts so that we can get access to the accounts and move the cash as much as we can to authorized depository institutions,” FTX’s new chief financial officer, Mary Cilia, speaking under oath, said during part of bankruptcy proceedings.

The management at FTX reportedly has no idea what is going on at the company.

The Chapter 11 bankruptcy hearings aim to wind up the exchange, but have been complicated by supposedly weak governance and poor record keeping under Bankman-Fried’s reign. The company’s new management were having to review customer terms and conditions that were stored in a variety of places such as Google Drive and Slack, Coverick said.

The company has still not filed a statement of assets or of its financial position required under U.S. bankruptcy law, and currently estimates it will be able to do so in April, Cilia said. The company is still trying to sort out how many employees it has worldwide – Cilia estimated the figure at 220 – and how much was withdrawn leading up to the bankruptcy.

We don’t even know how much they owe. We need to find someone who knows QuickBooks.

Dear Reader - The enemies of freedom are choking off the Gateway Pundit from the resources we need to bring you the truth. Since many asked for it, we now have a way for you to support The Gateway Pundit directly - and get ad-reduced access. Plus, there are goodies like a special Gateway Pundit coffee mug for supporters at a higher level. You can see all the options by clicking here - thank you for your support!

Dear Reader - The enemies of freedom are choking off the Gateway Pundit from the resources we need to bring you the truth. Since many asked for it, we now have a way for you to support The Gateway Pundit directly - and get ad-reduced access. Plus, there are goodies like a special Gateway Pundit coffee mug for supporters at a higher level. You can see all the options by clicking here - thank you for your support!